You checked your score. It says 700. That’s officially “good” — but is it good enough? A 700 credit score opens real doors: mortgages, car loans, solid credit cards. But the gap between 700 and 760 can cost you more than $50,000 in interest over a lifetime of borrowing. This guide breaks down exactly what a 700 score means today, what rates you’ll actually pay, and the fastest realistic path to push it higher.

What Does a 700 Credit Score Actually Mean?

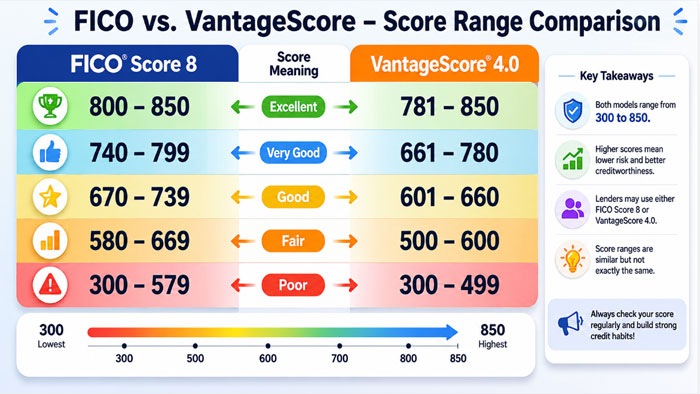

FICO vs. VantageScore: Two Scales, One Score

Most lenders use FICO Score 8 as their primary benchmark. Here’s how both major scoring models classify 700:

| Score Range | FICO Label | VantageScore Label |

|---|---|---|

| 300–579 | Poor | Very Poor (300–499) |

| 580–669 | Fair | Poor (500–600) |

| 670–739 | Good ← you’re here | Good (661–780) |

| 740–799 | Very Good | — |

| 800–850 | Exceptional | Excellent (781–850) |

Both models agree: 700 is solidly “good.” But neither model puts 700 in the top tier.

As of September 2025, the average FICO 8 score in the U.S. was 715. [FICO national average score data] The average VantageScore 3.0 stood at 697 as of February 2026. A 700 score puts you right at the national midpoint — which means you’re doing fine, but you’re not standing out to lenders.

Where 700 Ranks Among American Borrowers

About 21.6% of Americans sit in the 670–739 “good” range. Another 50%+ have crossed into “very good” or “exceptional” territory (740+). In practical terms: you’ll get approved for most products, but you won’t automatically qualify for the best rates. That distinction matters more than most people realize.

Is a 700 Credit Score Good Enough? The Honest Answer

Good enough to qualify? Usually yes. Good enough to get the lowest rate? Often no.

Lenders don’t just check if you clear their minimum threshold — they tier their interest rates by score. A 700 gets you through the door. A 760 gets you a better seat at the table. The difference isn’t abstract: it shows up as real dollars in your monthly payment.

Beyond the score itself, lenders also weigh your debt-to-income (DTI) ratio, income stability, employment history, and the age of your credit accounts. A 700 score with a 20% DTI is a much stronger application than a 700 score with a 45% DTI.

What Can You Get with a 700 Credit Score?

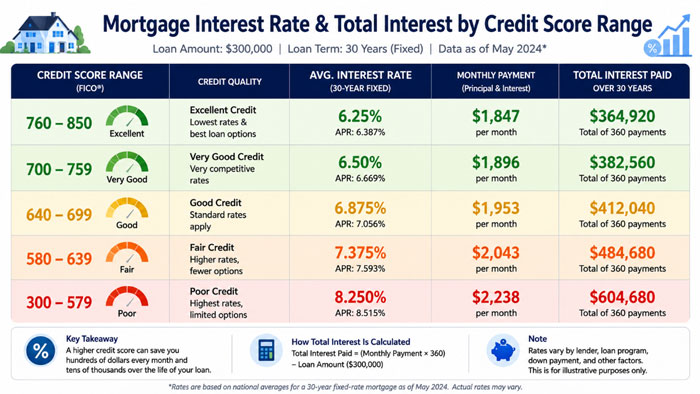

Mortgage Rates: Is 700 Good Enough to Buy a House?

Yes — a 700 credit score is sufficient to qualify for a conventional mortgage (minimum threshold is typically around 620). FHA loans are accessible at even lower scores. But “qualifying” and “getting a great rate” aren’t the same thing.

Here’s what the rate difference looks like on a $300,000, 30-year fixed mortgage (estimates based on 2025–2026 market conditions):

| Credit Score | Est. Rate | Monthly Payment | Total Interest (30yr) |

|---|---|---|---|

| 680–699 | ~7.2% | ~$2,039 | ~$434,000 |

| 700–719 | ~6.9% | ~$1,983 | ~$414,000 |

| 720–739 | ~6.6% | ~$1,928 | ~$394,000 |

| 740–759 | ~6.3% | ~$1,874 | ~$375,000 |

| 760+ | ~6.1% | ~$1,838 | ~$361,000 |

The math is stark: a 700 score vs. a 760 score on the same loan = roughly $53,000 more in interest over 30 years. That’s not a rounding error. That’s a car.

⚠️ Rates vary by lender, loan type, down payment, and state. Always compare at least three lenders before locking a rate.

how credit score affects mortgage approval and rates

Auto Loan Rates at 700

According to Experian’s Q4 2025 financing report, borrowers in the 661–780 score range paid an average of 6.27% on new vehicles and 9.98% on used vehicles. Nearly 69% of all financed vehicles in that period went to borrowers in this band or higher.

If you push your score above 740, you’ll typically qualify for the next tier down in rate — which on a $35,000 car loan over 60 months can save you $1,500–$2,500 in total interest.

Credit Cards You Can Actually Get

A 700 score puts most mainstream rewards cards within reach:

- Cash back cards (e.g., 1.5–2% flat-rate cards): accessible

- Travel rewards cards with solid sign-up bonuses: accessible

- 0% Intro APR cards (12–21 months): very likely accessible

- Premium cards (Amex Platinum, Chase Sapphire Reserve): typically require 740+

One practical tip: use prequalification tools before applying. Most issuers offer a soft inquiry precheck that won’t touch your score. Which brings us to an important concept a lot of borrowers get wrong.

Personal Loans

Most online lenders and banks will approve personal loans for 700+ borrowers. Expect APRs roughly in the 10–18% range depending on loan size, term, and lender. Compare offers using soft-pull prequalification before submitting a formal application.

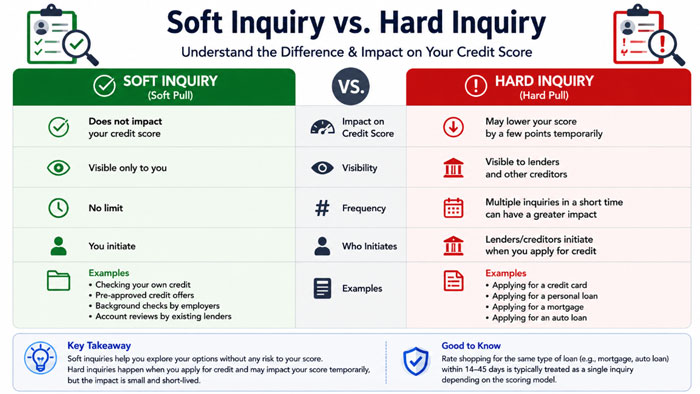

Soft Inquiry vs. Hard Inquiry: Know Before You Apply

This distinction trips up a surprising number of people — and costs them points.

| Soft Inquiry | Hard Inquiry | |

|---|---|---|

| Affects your score? | ❌ No | ✅ Yes (typically 2–5 pts) |

| Triggered by | Checking your own score, prequalification, employer checks | Formal loan/card applications |

| Stays on report | Not visible to lenders | Up to 2 years |

Rate shopping exception: If you’re applying for a mortgage, auto loan, or student loan, multiple hard inquiries within a 14–45 day window are typically counted as a single inquiry by FICO. So don’t avoid comparing lenders — just cluster your applications.

How to Go From 700 to 750: A Realistic Timeline

Getting from 700 to 750 is genuinely achievable within 6–12 months if you focus on the right levers.

The Two Factors That Move the Needle Most

Payment history (35% of your FICO score) is the single biggest factor. One 30-day late payment can drop a 700 score by 80–110 points. Set up autopay — at minimum for the minimum payment — on every account.

Credit utilization (30%) is the fastest thing you can actually change. Aim for under 10% across all cards, not just under 30%. If your total limit is $10,000, keep reported balances below $1,000. Pay before your statement closing date, not just before the due date — that’s when balances get reported to bureaus.

Your Improvement Timeline

| Action | Timeframe | Estimated Score Gain |

|---|---|---|

| Drop utilization from 30% → under 10% | 1–2 billing cycles | +20 to +40 pts |

| Request a credit limit increase | 30–60 days | +10 to +20 pts |

| Dispute and remove a credit report error | 30–45 days | +10 to +50 pts |

| 12 months of zero late payments | 12 months | +30 to +50 pts |

| Avoid new hard inquiries for 6 months | 6 months | +5 to +15 pts |

Don’t Skip Your Free Credit Reports

Pull your reports from all three bureaus annually at AnnualCreditReport.com — the only federally mandated free source. [free annual credit report access] Errors are more common than most people expect: incorrect account ownership, duplicate entries, outdated derogatory marks. Disputing a legitimate error can move your score meaningfully within 45 days.

step-by-step guide to disputing credit report errors

What Happens If You Miss a Payment at 700?

Know the three zones:

- 1–29 days late: No credit bureau report. You may owe a late fee or face a penalty APR — but your score is safe.

- 30+ days late: Officially reported. Score drop of 80–110 points is realistic for a 700-range borrower. This stays on your report for 7 years.

- 90+ days late: Serious delinquency. Collections risk. Significant multi-year damage.

The good news: a single 30-day late payment’s impact fades significantly after 18–24 months of clean payment history following it.

Frequently Asked Questions

Q: Is 700 a good credit score to buy a house in 2026?

Yes. You’ll qualify for conventional and FHA loans. But to access the best available mortgage rates, a score of 720–740+ is the more competitive target. The rate difference can add up to tens of thousands of dollars over the loan term.

Q: How long does it take to go from 700 to 750?

With focused effort on utilization and on-time payments, most people can reach 750 within 6–12 months. Removing a credit report error can accelerate this significantly.

Q: Will checking my own credit score hurt it?

No. Checking your own score is a soft inquiry and has zero impact on your credit. Use free tools from your bank, Credit Karma, or Experian to monitor regularly.

Q: Can I get a 0% APR credit card with a 700 credit score?

Most likely, yes. The majority of 0% intro APR cards target “good credit” borrowers (670+). Use prequalification tools to check your odds before applying formally.

Q: How much can I borrow with a 700 credit score?

Your score doesn’t determine your borrowing limit — your income and DTI ratio do. The score primarily determines whether you’re approved and what interest rate you pay.

What’s the fastest way to raise a 700 credit score?

The fastest lever: reduce your credit card utilization below 10% before your next statement date. Results typically appear within one billing cycle.

The Bottom Line

A 700 credit score is a real achievement — and a real starting point. You’ll get approved for mortgages, car loans, and strong credit cards. But the borrowers locking in the best rates sit above 740, often saving $40,000–$60,000 on a single mortgage. The gap is closeable. Most people in the 700 range are 6–12 months of consistent habits away from crossing into the next tier.

Pull your credit report. Identify what’s holding your score back. Then act on the one or two highest-impact changes first.

Once you hit 750, a different set of financial products becomes available — and the math changes considerably.

Disclaimer: The information in this article is for educational purposes only and does not constitute financial, legal, or investment advice. Credit score ranges, interest rates, and lending criteria vary by lender, loan type, location, and individual financial profile. Always consult a licensed financial advisor or credit counselor before making borrowing decisions. Rate estimates referenced are based on publicly available market data and are subject to change.