Frequently Asked Questions

Use our free car purchase vs. lease calculator to compare monthly payments, total loan costs, resale value, and maintenance. Get an instant, data-driven recommendation in seconds.

This calculator compares the true financial cost of buying versus leasing a vehicle over the same time period. Enter your car price, down payment, loan interest rate, and loan term for the purchase side. Then input your lease monthly payment, lease down payment, and lease term. The tool also factors in annual maintenance costs, estimated resale value, and expected mileage to calculate adjusted monthly costs and give you a data-driven recommendation.

Total Purchase Cost is the sum of all out-of-pocket expenses associated with buying the car — including your down payment, all monthly loan payments over the loan term, and cumulative maintenance costs — minus the car’s estimated resale value at the end of the comparable period. This gives you a realistic net cost of ownership, not just the sticker price.

Total Lease Cost includes your lease down payment plus all monthly lease payments over the full lease term. Unlike buying, your monthly payments go toward the vehicle’s depreciation during the lease period rather than building ownership equity, so there is no resale value to offset your costs at the end.

The standard monthly payment is your fixed loan installment. The Adjusted figure factors in additional ownership costs — primarily annual maintenance — spread over the loan term, minus any resale value recovered. It gives a more accurate picture of what buying actually costs you per month, making the comparison with leasing more apples-to-apples.

The average lease payment for a new car is $613 per month, compared to the average monthly loan payment of $767 for a purchased vehicle, so leasing typically offers lower monthly payments. However, this calculator also computes an adjusted monthly lease cost that accounts for the fact that you receive no asset or resale value at the end — which often makes leasing more expensive on a true per-month basis when viewed over time.

Mileage is a critical factor for leasing. Most leases restrict you to 10,000–15,000 miles per year and charge fees for excessive mileage at the end of the agreement. If you exceed your mileage limit by 2,000 miles and pay 30 cents per mile, you could owe an additional $600 at lease end. If you drive more than 15,000 miles annually, buying is generally the more cost-effective option. This calculator lets you select your expected mileage level to reflect that in the comparison.

Resale value varies significantly by make, model, and condition. Most new cars lose around 20% of their value in the first year and up to 60% over five years. Reliable sources like Kelley Blue Book (KBB) and Edmunds publish depreciation estimates by model year. As a general starting point, a 40% residual value after five years is reasonable for mainstream vehicles, though luxury cars often depreciate faster and certain brands (Toyota, Honda) retain value better.

Buying tends to be the better financial choice when: 1.You plan to keep the car for 5 or more years 2.You drive more than 15,000 miles per year 3.You want to build equity and eventually eliminate monthly payments 4.You want freedom to customize or modify the vehicle You live in a rural area with limited public transport and rely heavily on your car.

Leasing is often the smarter move when you want lower monthly payments, prefer driving a new vehicle every few years, and don’t want to worry about long-term maintenance costs. It’s also worth considering if you want to test-drive an EV lifestyle before committing to purchase, or if your employer offers vehicle-related tax benefits for leased cars.

This calculator focuses on the core financial comparison: loan payments, lease payments, down payments, maintenance, and resale value. It does not currently include sales tax rates, insurance premiums, or potential lease-end wear-and-tear charges. For a complete picture, add your local tax rate and insurance quotes to the totals shown.

Yes. Simply enter the actual purchase price of the used car or EV, along with the applicable loan rate and lease terms if you have them. For EVs, keep in mind that some manufacturers are offering their own incentives to replace the federal EV tax credit that ended in September 2025, which may lower your effective lease or purchase price — adjust your input figures accordingly.

The recommendation is based on a quantitative comparison of total adjusted costs over the lease term. It reflects the mathematical outcome given your inputs — it does not account for personal factors like job flexibility, credit score impact, or lifestyle preferences. Use it as a reliable financial baseline, then factor in your individual circumstances before making a final decision.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

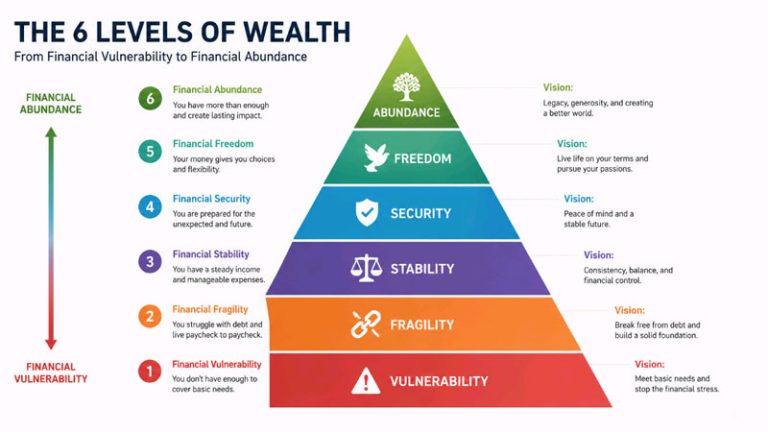

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…