Frequently Asked Questions

File Schedule C easily with our free tool. Report sole proprietor business income, expenses, deductions & net profit/loss accurately. Trusted by freelancers & small business owners.

Schedule C is required for sole proprietors and single-member LLCs who earned income from a business or side gig during the tax year. If you received a 1099-NEC or ran a freelance operation, you almost certainly need it.

It’s a 6-digit code assigned by the IRS that classifies your type of business activity (e.g., consulting, retail, food service). You can find the correct code in the IRS Schedule C instructions or the NAICS code lookup table.

An EIN (Employer Identification Number) is a federal tax ID issued by the IRS. Sole proprietors without employees can use their Social Security Number instead — the EIN field on Schedule C is optional unless you have hired employees or operate under a formal business entity.

Under the Cash method, you report income when received and expenses when paid — the most common choice for small businesses. Under the Accrual method, you record income when earned and expenses when incurred, regardless of when money actually changes hands.

Gross Income = (Gross Receipts or Sales) − (Returns & Allowances) − (Cost of Goods Sold) + Other Income. This figure represents your total business revenue before any operating expenses are deducted.

Deductible expenses include advertising, car and truck expenses, commissions and fees, contract labor, depreciation, insurance (non-health), mortgage and other interest, legal and professional services, office expenses, rent or lease payments, repairs and maintenance, supplies, taxes and licenses, travel, meals (subject to the 50% limit), utilities, wages, and other ordinary and necessary business costs.

You enter total qualifying meal expenses under “Meals,” and the tool automatically calculates the deductible portion (generally 50%) in the “Deductible meals” field below, in line with IRS rules.

If you use part of your home exclusively and regularly for business, you may deduct a proportional share of housing costs. This deduction is entered in Part III and reduces your Tentative Profit to arrive at your final Net Profit or Loss.

Net Profit (or Loss) = Gross Income − Total Expenses − Home Office Deduction. A positive number is taxable self-employment income; a negative number may offset other income on your Form 1040.

Complete Part IV only if you are claiming car and truck expenses in Part II. You will need to provide the vehicle description, the date it was placed in service, business miles, commuting miles, other personal miles, and whether the vehicle was available for personal use during off-duty hours.

Yes. The “Other Expenses” section allows you to enter additional business expenses not covered by the standard categories. Each entry requires a description and a dollar amount — up to two additional line items are supported in this form.

No. Those fields are auto-calculated based on your inputs and are read-only. This ensures mathematical accuracy and reduces filing errors.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

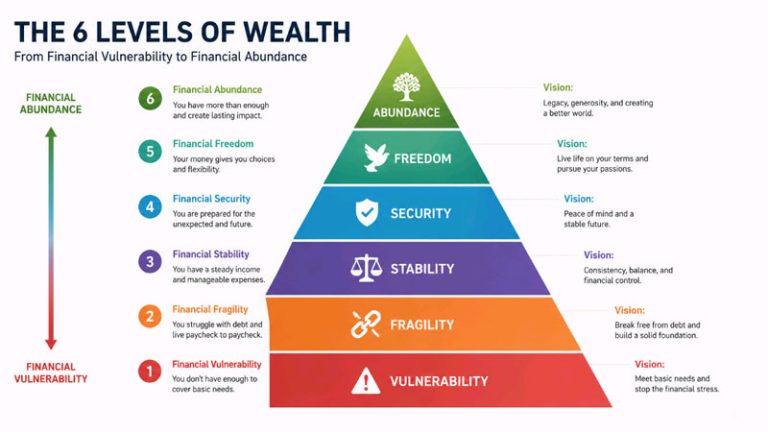

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…