Roth Ira Compound Interest Calculator

Free Roth IRA growth calculator: estimate your balance at retirement, compare Roth vs. taxable account returns, and plan contributions using 2025 IRS rules.

Frequently Asked Questions

See how much your Roth IRA could grow by retirement. Enter your age and contributions — our free calculator shows your projected balance and tax savings instantly.

A Roth IRA (Individual Retirement Account) is a tax-advantaged retirement savings account funded with after-tax dollars. Unlike a Traditional IRA, contributions are not tax-deductible — but your money grows completely tax-free, and qualified withdrawals in retirement are also tax-free.

To make a qualified withdrawal, you generally must be at least 59½ years old and have held the account for at least five years. Because taxes are paid upfront, a Roth IRA is especially powerful for younger savers who expect to be in a higher tax bracket later in life.

The IRS sets annual contribution limits that apply to the total of all your IRAs combined:

| Tax Year | Under Age 50 | Age 50 or Older (with catch-up) |

|---|---|---|

| 2025 | $7,000 | $8,000 |

| 2026 | $7,500 | $8,600 |

Important: You cannot contribute more than your earned income for the year. If you earned $4,000 in 2025, your maximum contribution is $4,000 — not $7,000.

Yes. Your ability to contribute to a Roth IRA phases out at higher income levels, based on your Modified Adjusted Gross Income (MAGI):

2025 income phase-out ranges:

- Single filers / Head of household: $150,000–$165,000

- Married filing jointly: $236,000–$246,000

- Married filing separately: $0–$10,000

2026 income phase-out ranges:

- Single filers: $153,000–$168,000

- Married filing jointly: $242,000–$252,000

If your income is above the upper limit, you cannot make a direct Roth IRA contribution. However, a “backdoor” Roth IRA conversion (converting a non-deductible Traditional IRA to a Roth) is a legal strategy many high earners use — consult a tax advisor for guidance.

Our calculator uses the following inputs to project your retirement balance:

- Starting balance — Any existing savings already in your IRA

- Current age & retirement age — Determines how many years your money compounds

- Annual contribution — How much you add each year (or select “Maximize” to use the IRS limit)

- Expected rate of return — The historical average annual return of the S&P 500 is approximately 7–10%; our default is 7% (inflation-adjusted)

- Marginal tax rate — Used to calculate the after-tax growth rate of the comparison taxable account

The calculator then projects two growth curves year by year:

- Roth IRA — grows at your full rate of return, tax-free

- Taxable account — grows at your rate of return reduced by your annual tax rate (return × (1 − tax rate))

The difference between the two lines illustrates the tangible dollar value of tax-free compounding over time.

A taxable brokerage account has no special tax protections — dividends, interest, and capital gains are taxed each year. This reduces the effective annual growth rate, which significantly lowers your ending balance over decades.

For example, at a 7% gross return with a 25% marginal tax rate:

- Roth IRA effective rate: 7.00% (tax-free)

- Taxable account effective rate: ~5.25% (7% × 75%)

Over 36 years, this difference can amount to hundreds of thousands of dollars — which is exactly what the chart in our calculator visualizes.

Selecting Yes tells the calculator to automatically use the IRS annual maximum ($7,000 for under-50, $8,000 for age 50+) instead of your manually entered contribution amount. This is useful if you want to see the best-case scenario assuming you always contribute the legal maximum each year.

Yes. Having an employer-sponsored plan like a 401(k) does not prevent you from contributing to a Roth IRA, as long as your income stays within the Roth IRA MAGI limits. The two accounts have separate contribution limits and can be used simultaneously to diversify your tax exposure in retirement (pre-tax 401(k) withdrawals vs. tax-free Roth withdrawals).

Roth IRA withdrawal rules differ depending on whether you’re withdrawing contributions or earnings:

- Contributions (money you put in): Can be withdrawn at any time, tax-free and penalty-free, because they were already taxed.

- Earnings (investment growth): Must meet two conditions for a qualified (tax-free, penalty-free) withdrawal:

- You are at least 59½ years old, AND

- The account has been open for at least 5 years

Exceptions to the 10% early withdrawal penalty on earnings include:

- First-time home purchase (up to $10,000 lifetime)

- Permanent disability

- Qualified higher education expenses

- Health insurance premiums while unemployed

- Substantially Equal Periodic Payments (SEPP / Rule 72(t))

No — this is one of the most significant advantages of a Roth IRA. Unlike Traditional IRAs and 401(k)s, Roth IRAs have no Required Minimum Distributions during the owner’s lifetime. This means you can leave the money to grow indefinitely, making the Roth IRA an excellent wealth-transfer and estate-planning tool in addition to a retirement vehicle.

Note: Inherited Roth IRAs are subject to RMD rules for non-spouse beneficiaries under the SECURE 2.0 Act.

There is no universal answer — the right choice depends on your personal tax situation:

| Scenario | Better Choice |

|---|---|

| You expect to be in a higher tax bracket in retirement | Roth IRA |

| You want a tax deduction now and expect lower taxes later | Traditional IRA |

| You’re young with decades of compounding ahead | Roth IRA |

| You need to reduce taxable income this year | Traditional IRA |

| You want no RMDs and flexible estate planning | Roth IRA |

Many financial planners recommend contributing to both when possible to create tax diversification — giving you flexibility to draw from different buckets in retirement based on your tax situation each year.

The rate of return you enter should reflect your expected average annual investment growth. Common reference points:

- S&P 500 historical average: ~10% nominal / ~7% inflation-adjusted (long-term)

- Conservative (bonds-heavy portfolio): 4–5%

- Moderate (balanced portfolio): 6–7%

- Aggressive (stock-heavy): 8–10%

Our calculator defaults to 7% — a widely used, inflation-adjusted benchmark. Keep in mind that past performance does not guarantee future results, and actual returns will vary year to year.

Excess contributions are subject to a 6% excise tax per year for every year the excess amount remains in the account. To avoid this penalty, you must withdraw the excess contributions (plus any earnings on them) by your tax filing deadline (including extensions).

If you’ve already filed your taxes, you can still remove excess contributions by October 15 of the following year without amending your return in many cases. Consult a tax professional if you’ve made excess contributions.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

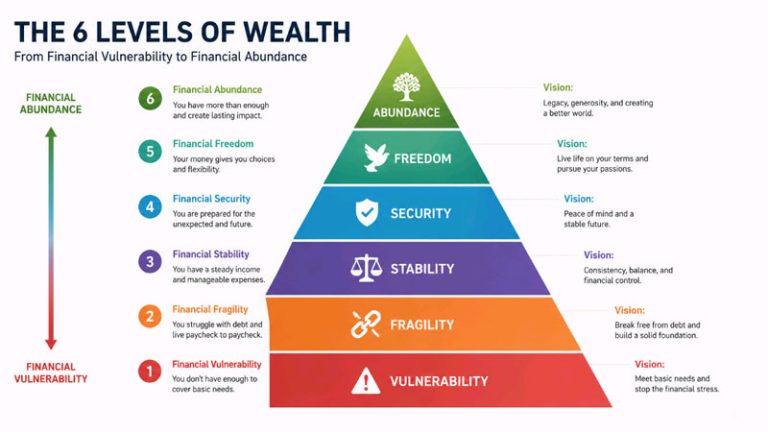

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…