Calculate Your Credit Card Debt Fast

Enter your balance and interest rate to estimate your payoff timeline and total interest paid.

Fill in the details and click Calculate

Frequently Asked Questions

Free credit card payoff calculator: enter your balance, APR, and monthly payment to instantly see your payoff date, total interest, and money-saving alternatives.

The calculator uses the standard amortization formula to compute how long it takes to pay off your balance given a fixed monthly payment and annual percentage rate (APR). Each month, your APR is divided by 12 to get the monthly interest rate. Interest is applied to your remaining balance first; the rest of your payment reduces the principal. The formula used is:

n = –log(1 – (r × P) / M) / log(1 + r)

Where P = balance, r = monthly interest rate (APR ÷ 12), M = monthly payment, and n = number of months to pay off. This is the same method used by banks and credit card issuers.

APR stands for Annual Percentage Rate — the yearly interest rate charged on your outstanding credit card balance. It matters because even a few percentage points of difference can cost or save you hundreds of dollars over time. For example, on a $3,500 balance:

- At 21% APR with $151/month → you pay ~$1,025 in interest over 30 months

- At 15% APR with $151/month → you pay ~$680 in interest over 27 months

Always use your card’s purchase APR (not the promotional or cash advance rate) for the most accurate estimate. You can find your APR on your monthly statement or your card’s terms and conditions.

Credit card issuers typically require a minimum payment of 1–3% of your outstanding balance or a small fixed dollar amount, whichever is greater. Paying only the minimum is one of the most expensive financial habits you can have. Here’s why:

- On a $3,500 balance at 21% APR, paying the minimum (~$70/month) could take over 7 years and cost more than $2,800 in interest — nearly doubling what you originally owed.

- Paying $151/month instead clears the same debt in just 30 months and saves over $1,700 in interest.

As a rule of thumb: always pay at least 2–3× the minimum, or as much as you can comfortably afford each month.

A balance transfer card lets you move existing high-interest credit card debt to a new card that offers a 0% introductory APR — typically for 12 to 21 months. During that period, every dollar you pay goes directly toward reducing your principal, with zero interest charges.

It makes sense if:

- You have a good credit score (typically 670+) to qualify

- You can realistically pay off the balance within the 0% promotional period

- The balance transfer fee (usually 3–5% of the amount transferred) is less than the interest you’d otherwise pay

Watch out for:

- The regular APR after the promotional period ends (often 20–29%)

- Continuing to spend on the new card while paying off the transferred balance

Using our calculator’s comparison tool, you can instantly see how much a 0% balance transfer would save you versus your current card.

A personal loan is an installment loan with a fixed interest rate, fixed monthly payment, and a defined end date. Credit cards are revolving debt with variable minimum payments and no fixed payoff date.

| Credit Card | Personal Loan | |

|---|---|---|

| Typical APR | 18–28% | 7–15% |

| Monthly payment | Variable | Fixed |

| Payoff date | Open-ended | Defined |

| Impact on credit | High utilization | Installment mix |

For most borrowers with a balance over $2,000 and a credit score above 650, a personal loan at 8–12% APR can significantly reduce both monthly payments and total interest paid. Our calculator shows this comparison automatically once you run your numbers.

Use the “By Months to Pay Off” mode in our calculator to get an exact figure. As a general reference, here are the required monthly payments for a $3,500 balance at 21% APR:

| Target Payoff | Monthly Payment | Total Interest |

|---|---|---|

| 12 months | ~$325 | ~$400 |

| 18 months | ~$228 | ~$605 |

| 24 months | ~$180 | ~$823 |

| 30 months | ~$151 | ~$1,025 |

The faster you pay, the less interest you pay — it’s as simple as that. Even increasing your monthly payment by $20–$30 can save hundreds of dollars and shave months off your payoff timeline.

Yes — and significantly so. Your credit utilization ratio (the percentage of your available credit you’re using) accounts for approximately 30% of your FICO score. Paying down your balance directly lowers this ratio.

General benchmarks:

- Below 30% utilization — considered good

- Below 10% utilization — considered excellent

For example, if your credit limit is $5,000 and your balance is $3,500, your utilization is 70% — well above the recommended threshold. Paying it down to $1,500 (30%) or $500 (10%) can noticeably boost your score within one or two billing cycles.

Note: Credit score impacts vary by individual. This calculator does not access or affect your credit report.

Our calculator produces accurate estimates based on standard financial math, with the following assumptions:

- Fixed APR — your interest rate does not change during the payoff period

- Fixed monthly payment — you pay the same amount every month

- No new purchases — no additional charges are added to the balance

- Interest compounded monthly — consistent with how most U.S. credit card issuers calculate interest

In reality, your actual payoff may vary slightly due to daily interest compounding (some issuers charge interest daily), changes in your APR, or irregular payments. For exact figures, always consult your card issuer or a certified financial advisor.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

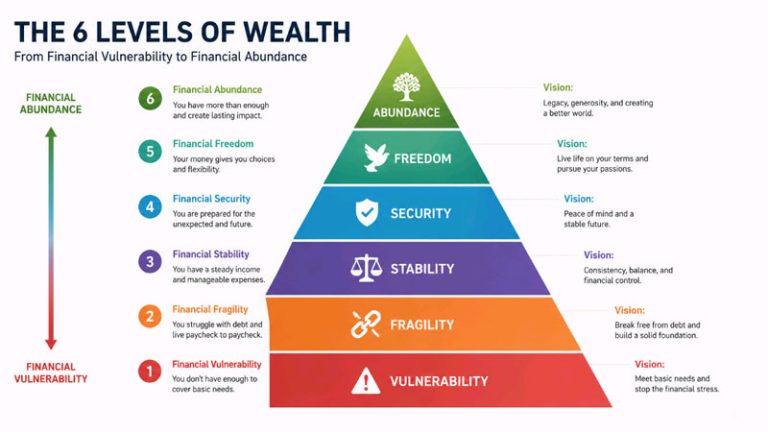

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…