Frequently Asked Questions

Use our free Form 1040 calculator to estimate your U.S. federal income tax liability. Enter income, deductions, and credits to instantly calculate your refund or balance due.

Form 1040 is the standard U.S. federal income tax return form used by individual taxpayers to report annual income, claim deductions and credits, and calculate their tax liability or refund. Most U.S. citizens and permanent residents with taxable income are required to file Form 1040 each year with the IRS.

Form 1040 supports five filing statuses: Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Surviving Spouse. Your filing status affects your standard deduction amount, tax bracket, and eligibility for certain credits. Selecting the correct status is critical to an accurate return.

You must report all sources of taxable income, including wages, salaries and tips (from Form W-2), interest income, dividend income, business income or loss (Schedule C), capital gains or losses (Schedule D), IRA distributions, pension and annuity payments, Social Security benefits, and other income such as unemployment compensation, prizes, or gambling winnings.

Up to 85% of your Social Security benefits may be taxable depending on your total income. The IRS uses your “combined income” (AGI + nontaxable interest + 50% of Social Security benefits) to determine the taxable portion. Our calculator applies the 85% taxable rate standard used in the Form 1040 computation.

AGI is your total gross income minus specific adjustments. Common adjustments include educator expenses (up to $300), IRA contributions, student loan interest deductions (up to $2,500), the deductible portion of self-employment tax, and health savings account (HSA) deductions. AGI is a key figure — it determines your eligibility for many deductions and credits.

For tax year 2023, the standard deduction is $13,850 for Single filers. You should itemize deductions (using Schedule A) only if your total eligible expenses — such as mortgage interest, state taxes, and charitable contributions — exceed the standard deduction amount for your filing status. Most taxpayers benefit from taking the standard deduction.

Form 1040 allows you to claim several valuable credits that directly reduce your tax bill, including: Child Tax Credit, Credit for Other Dependents, Education Credits (American Opportunity & Lifetime Learning), Retirement Savings Contribution Credit (Saver’s Credit), foreign tax credits, and energy credits. Unlike deductions, credits reduce your tax dollar-for-dollar.

A tax deduction reduces your taxable income, which indirectly lowers your tax bill based on your marginal tax rate. A tax credit directly reduces the amount of tax you owe, dollar-for-dollar. For example, a $1,000 deduction saves you $220 if you’re in the 22% bracket, while a $1,000 tax credit saves you exactly $1,000 regardless of your bracket.

Beyond regular income tax, you may also owe: Self-Employment Tax (Schedule SE), Additional Medicare Tax (Form 8959, for high earners), Net Investment Income Tax (Form 8960, 3.8% on investment income above thresholds), and household employment taxes or repayment of certain credits. These are reported in the “Other Taxes” section of Form 1040.

Your refund or balance due is determined by comparing your Total Tax against your Total Payments. Payments include federal income tax withheld (from W-2s and 1099s), estimated tax payments, and refundable credits such as the Earned Income Credit, Additional Child Tax Credit, American Opportunity Credit, and Recovery Rebate Credit. If payments exceed total tax owed, you receive a refund. If total tax exceeds payments, you owe the difference.

Your effective tax rate is your total federal tax liability divided by your total gross income, expressed as a percentage. It reflects the actual average rate at which your income is taxed — and is typically lower than your marginal (highest bracket) rate, because the U.S. uses a progressive tax system where different portions of income are taxed at different rates.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

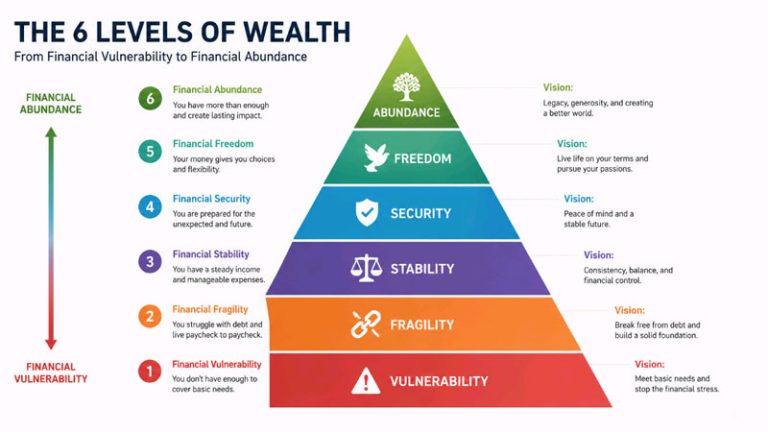

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…