Frequently Asked Questions

Not sure how much life insurance you need? Our expert-built Life Insurance Calculator gives you a personalized coverage estimate in seconds — based on your age, income, dependents, and current liabilities.

Our calculator uses key personal and financial inputs — including your age, annual income, number of dependents, and current liabilities — to estimate the amount of life insurance coverage you may need. The result is based on widely recognized financial planning methodologies, such as the income replacement and DIME (Debt, Income, Mortgage, Education) approaches.

A common rule of thumb is to have coverage equal to 10–15 times your annual income. However, your ideal coverage depends on multiple factors: the number of people financially dependent on you, outstanding debts (mortgages, loans, credit cards), future expenses such as education costs, and your existing savings or assets. Our calculator factors in these variables to give you a more personalized estimate.

Yes. The information you enter — including your name, income, and email — is used solely to generate your coverage estimate and, if you choose, to deliver results to your inbox. We do not sell or share your data with third parties. Please refer to our Privacy Policy for full details.

The two most common types are Term Life Insurance — provides coverage for a fixed period (e.g., 10, 20, or 30 years) and is generally more affordable and straightforward, making it suitable for most families, and Whole Life Insurance — offers lifelong coverage and includes a cash value component that grows over time, though premiums are significantly higher. The right type depends on your financial goals, budget, and how long you need coverage, and a licensed financial advisor can help you evaluate your options.

Current liabilities refer to debts and financial obligations you carry — such as a mortgage, car loans, student loans, or credit card balances. In the event of your passing, these debts do not simply disappear; they may become a burden for your family or estate. Including your liabilities in the calculation ensures your coverage is sufficient to settle outstanding obligations in addition to replacing your income.

Absolutely. Each dependent — whether a child, a spouse who does not work, or an aging parent — represents an ongoing financial responsibility. The more dependents you have, the greater the coverage you typically need to ensure their financial security over the long term.

No. This tool is designed to provide an educational estimate to help you understand your potential insurance needs. It does not constitute financial, legal, or insurance advice. We strongly recommend consulting a licensed financial planner or insurance professional before making any coverage decisions.

You should reassess your coverage whenever a major life event occurs, including marriage or divorce, birth or adoption of a child, purchasing a home, significant change in income, or retirement planning, and as a general best practice, reviewing your coverage every 3–5 years ensures it remains aligned with your current financial situation.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

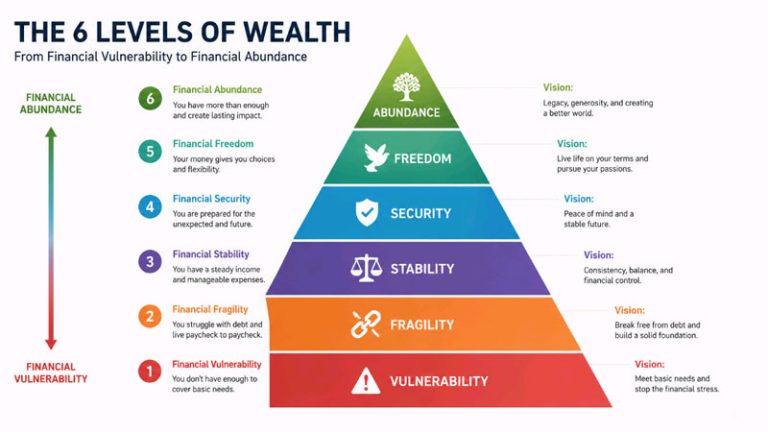

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…