Frequently Asked Questions

Plan your auto loan with our car payment calculator. Compare interest rates, loan terms & down payments to make informed car financing decisions today.

This calculator uses your car price, initial deposit, down payment percentage, loan term, and annual interest rate to compute your monthly payment using the standard amortizing loan formula. If you’re trading in a vehicle, that value is also factored into the loan amount, giving you a precise breakdown of total interest paid and total repayment cost.

An initial deposit is an upfront amount paid to reserve or secure the vehicle — it may or may not apply toward the purchase price. A down payment is a percentage of the car’s price paid at the time of purchase, directly reducing the loan amount you need to finance. Understanding both helps you negotiate better terms at the dealership.

Monthly payments are calculated using the standard amortization formula: M = P × [r(1+r)ⁿ] / [(1+r)ⁿ – 1], where P is the loan principal (car price minus deposit and down payment), r is the monthly interest rate (annual rate divided by 12), and n is the total number of monthly payments (loan term in years multiplied by 12).

Interest rates vary by credit score, lender, and market conditions. As a general benchmark, excellent credit (720+) typically gets 4%–6% APR, good credit (660–719) 6%–9% APR, fair credit (580–659) 10%–15% APR, and poor credit (below 580) 15%–20%+ APR. Always compare offers from multiple lenders — banks, credit unions, and dealership financing — before committing.

Your trade-in vehicle’s value is applied as a credit toward your new car purchase, effectively reducing the loan principal. For example, if your car costs $30,000 and your trade-in is worth $8,000, your financed amount before other deposits becomes $22,000. This can significantly lower your monthly payments and total interest paid.

Financial experts generally recommend a down payment of at least 20% for new cars and 10% for used cars. A larger down payment means a smaller loan, lower monthly payments, less interest paid over time, and a reduced risk of becoming “upside down” (owing more than the car is worth).

Shorter loan terms (24–48 months) mean higher monthly payments but significantly less interest paid overall. Longer terms (60–84 months) reduce monthly costs but increase total repayment. Most financial advisors recommend keeping auto loans to 60 months or fewer to avoid excessive interest accumulation and depreciation risk.

Your email is collected so a financing summary or quote can be sent directly to you for reference. This allows you or your dealer to revisit the figures without recalculating. Your information is used solely for this purpose and is not shared with third parties.

No. This is a planning tool only — no credit inquiry is made when you use the calculator. Your credit score is only affected when a lender performs a hard inquiry as part of a formal loan application.

The calculator provides highly accurate estimates based on the inputs you provide. Actual loan offers from lenders may vary due to origination fees, taxes, registration costs, insurance requirements, or lender-specific rate adjustments. Use this tool as a reliable starting point for your financing negotiations.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

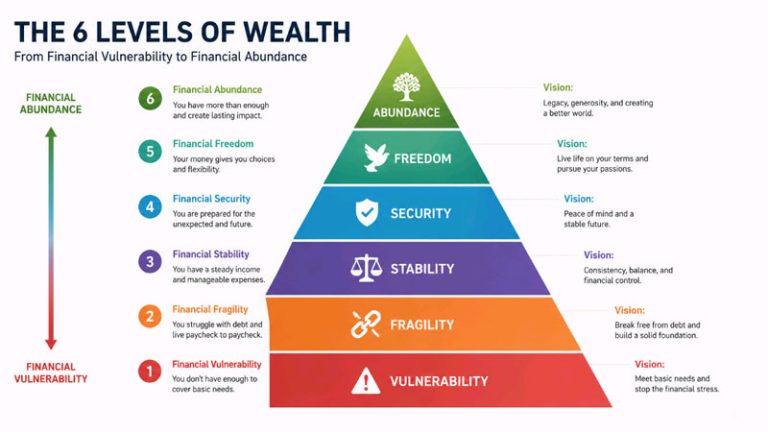

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…