The average new car now costs $48,401. The average used car? $28,000+. If you’re trying to figure out how to save money for a car without derailing your finances, the math matters more than the motivation. This guide gives you a concrete, step-by-step system — from setting a realistic savings target to protecting your credit score — so you can buy smart, not just fast.

Why Saving Upfront Beats Borrowing Everything

Before we get into tactics, let’s settle the “why bother saving?” question.

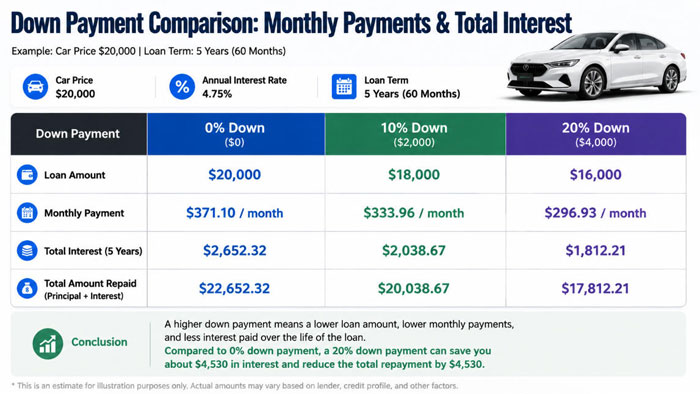

A $30,000 auto loan at 7.5% APR over 60 months costs you roughly $6,100 in interest alone. Put 20% down ($6,000), and that same loan drops to $24,000 — saving you nearly $2,000 in interest and cutting your monthly payment by about $100.

That’s not a small difference. That’s a vacation, three months of groceries, or a solid emergency fund.

Cars are depreciating assets. A new vehicle loses roughly 20% of its value in the first year. The less you borrow against something that’s falling in value, the better your financial position.

Step 1: Set a Target Number, Not Just a Vague Goal

“Save money for a car” is not a plan. A number is.

Here’s how to calculate yours:

- Pick your target vehicle. Research current market prices on Edmunds or KBB. Be honest about new vs. used.

- Set a down payment target. Aim for at least 10–20% of the purchase price. For a $25,000 used car, that’s $2,500–$5,000.

- Add purchase costs. Sales tax varies widely by state — Oregon charges 0%, California charges up to 10.25%. Factor in registration fees ($100–$500) and your first month of insurance.

- Add a buffer. Build in an extra $500–$1,000 for unexpected pre-purchase costs like a pre-purchase inspection or dealer fees.

Quick example: $25,000 car × 20% down = $5,000 + $1,800 in taxes/fees + $500 buffer = $7,300 savings target.

Now you have something to work toward.

Step 2: Know How Long It Will Actually Take

This is where most buyers stall — they underestimate the timeline and give up.

| Monthly Savings | $5,000 Target | $7,500 Target | $10,000 Target |

|---|---|---|---|

| $300/month | 17 months | 25 months | 34 months |

| $500/month | 10 months | 15 months | 20 months |

| $800/month | 7 months | 10 months | 13 months |

Pick a timeline that’s uncomfortable but realistic. Then work backward to find the monthly number.

monthly budget planner for large purchases

Step 3: Open a Dedicated High-Yield Savings Account

This one step eliminates most “I spent the money on something else” excuses.

Open a separate savings account used only for your car fund. Don’t link it to your checking debit card. Out of sight, out of mind.

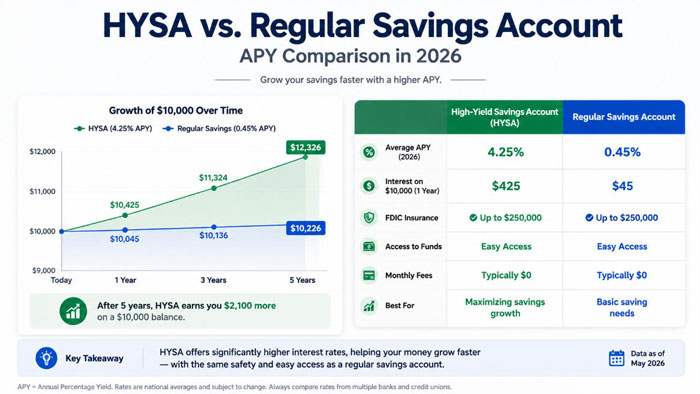

Better yet, open a High-Yield Savings Account (HYSA). As of early 2026, top HYSAs are paying 4.5–5.0% APY — versus the national average of around 0.46% APY for standard savings accounts.

On a $6,000 balance saved over 12 months, that difference adds up to roughly $270 in free interest. Not life-changing, but it’s money you didn’t have to earn.

Set up automatic transfers on payday. Even $200 bi-weekly adds up to $5,200 a year before you think about touching it.

FDIC-insured deposit account protections

Step 4: Cut Expenses — But Be Strategic About It

Don’t try to cut everything at once. That approach burns people out in week two.

Instead, run a subscription audit. List every recurring charge hitting your accounts this month. According to the Bureau of Labor Statistics’ Consumer Expenditure Survey, the average American household spends over $3,200 annually on entertainment and personal services — much of it on subscriptions they’ve forgotten about.

Cancel or pause what you don’t use weekly. Redirect that money directly to your car fund.

Next, target your top three spending categories outside of rent and utilities. For most people, that’s dining out, groceries, and shopping. A realistic 20–30% reduction in discretionary spending can free up $200–$400/month without feeling like deprivation.

The 50/30/20 rule is a useful framework here: 50% of take-home pay on needs, 30% on wants, 20% on savings. During your car-saving sprint, consider shifting that to 50/20/30 — squeezing wants to free up more for savings.

Step 5: Accelerate With One-Time Income Injections

Steady monthly savings build the foundation. Lump sums accelerate it.

Tax refunds: The IRS reports the average federal tax refund is around $3,167. If you’re expecting one, commit it to your car fund before it hits your checking account.

Sell what you don’t use: Facebook Marketplace, eBay, and OfferUp are legitimate tools. A weekend of decluttering can realistically generate $300–$800.

Side income: For the 28–45 age bracket, the most accessible options are freelance work in your professional field, rideshare driving, or renting out a parking space or storage area. Even $200–$300/month in side income shaves months off your timeline.

Step 6: Don’t Ignore Your Credit Score While You Save

Here’s the part most car-saving guides skip entirely — and it costs buyers thousands.

Your credit score doesn’t just determine if you get approved for a loan. It determines what rate you pay.

| Credit Score Range | Avg. New Car Rate | Avg. Used Car Rate |

|---|---|---|

| 781–850 (Super Prime) | ~5.1% | ~5.8% |

| 661–780 (Prime) | ~6.7% | ~9.1% |

| 601–660 (Nonprime) | ~9.8% | ~13.8% |

| 501–600 (Subprime) | ~12.9% | ~18.9% |

Source: Experian State of the Automotive Finance Market

The gap between a Super Prime and Subprime rate on a $25,000 loan (60 months) is over $6,000 in additional interest. That’s more than most people save for a down payment.

While you’re saving, focus on:

- Paying every bill on time (payment history = 35% of your FICO score)

- Keeping credit card utilization below 30%

- Pulling your free report at AnnualCreditReport.com to catch any errors

how to improve your credit score before a major purchase

Step 7: Know the Real Cost of Ownership Before You Buy

Your savings goal shouldn’t stop at the down payment.

According to AAA’s annual “Your Driving Costs” report, the average annual cost of owning and operating a new vehicle is now over $12,000/year — roughly $1,000/month when you factor in loan payments, insurance, fuel, maintenance, and registration.

Before you finalize your target car, run this quick check:

- Insurance estimate: Get quotes before you fall in love with a vehicle. Sports cars and newer models cost significantly more to insure.

- Fuel costs: Compare MPG and calculate your monthly fuel bill at current gas prices.

- Maintenance: Used cars outside warranty can have unpredictable repair costs. Budget $500–$1,000/year as a baseline.

A car you can technically afford to buy but can’t comfortably afford to own is a budget problem, not just a math problem.

FAQ: How to Save Money for a Car

Aim for at least 10–20% of the vehicle’s purchase price as a down payment, plus enough to cover taxes, registration, and the first month of insurance. A $25,000 car typically requires $4,000–$7,000 out of pocket before you drive off the lot.

Both, ideally. A loan lets you buy sooner; a larger down payment reduces your total borrowing cost. The sweet spot is saving a meaningful down payment (10–20%) while maintaining a strong credit score to qualify for a competitive interest rate.

At $500/month, about 10 months. At $300/month, roughly 17 months. Using a tax refund or selling assets can meaningfully shorten the timeline.

20% is the standard recommendation. If that’s out of reach, 10% is a workable floor — just expect higher monthly payments and more total interest paid over the loan term.

No. Your emergency fund and your car fund should be entirely separate. Draining your emergency savings to buy a car leaves you financially exposed the moment something goes wrong — and something always does.

Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or legal advice. Interest rates, vehicle prices, and tax figures referenced are approximate and subject to change. Please consult a licensed financial advisor or certified financial planner (CFP) for guidance tailored to your individual circumstances.