Introduction

Figuring out how to save money for a house is one of the hardest financial challenges for working Americans today. Home prices remain near historic highs — the national median hit $407,200 in late 2024, according to the National Association of Realtors. For most first-time buyers, the gap between wanting a home and affording one feels enormous.

It doesn’t have to stay that way.

This guide gives you a clear, realistic savings plan — covering down payments, closing costs, credit scores, and government programs most buyers never use.

Why Saving for a House Is Harder Than It Looks

Before you build a plan, you need to know the real number — and it’s almost always bigger than buyers expect.

Most people budget for the down payment and forget everything else.

The True Cost of Buying a Home

Here’s what you actually need in cash on closing day for a $350,000 home:

| Cost Item | Estimated Range |

|---|---|

| Down Payment (10%) | $35,000 |

| Closing Costs (2–5%) | $7,000 – $17,500 |

| Home Inspection | $300 – $500 |

| Moving Costs | $1,000 – $3,000 |

| 3-Month Mortgage Reserve | ~$5,000 |

| Total Cash Needed | ~$48,000 – $61,000 |

This is why a savings plan that only targets the down payment sets you up to fall short at the finish line.

〔E-E-A-T Data Point〕 According to the CFPB, nearly 1 in 3 first-time buyers are surprised by closing costs. Budget for them from Day 1.

How Much Do You Actually Need to Save?

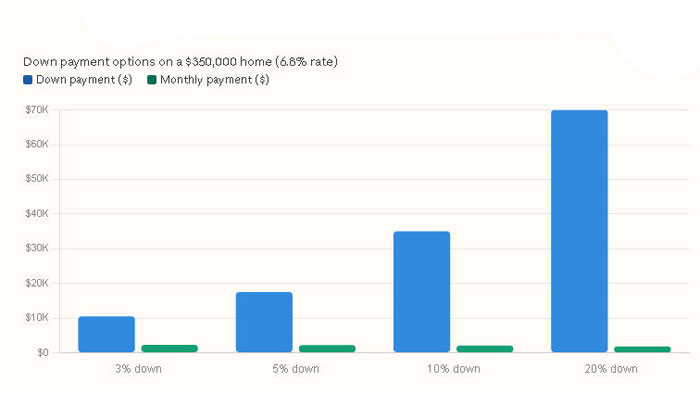

Choosing the Right Down Payment Percentage

The 20% down payment is not a rule — it’s a benchmark. Here’s what different down payment levels actually mean for your monthly payment on a $350,000 home (estimated at a 6.8% rate):

| Down Payment | Amount | PMI Required? | Est. Monthly Payment |

|---|---|---|---|

| 3% | $10,500 | Yes | ~$2,320 |

| 5% | $17,500 | Yes | ~$2,240 |

| 10% | $35,000 | Yes (reduced) | ~$2,090 |

| 20% | $70,000 | No | ~$1,820 |

PMI typically costs 0.5%–1.5% of your loan amount per year — on a $315,000 loan, that’s $130–$390 added to your monthly bill until you reach 20% equity.

Putting 20% down saves real money over time. But waiting five extra years to save that amount while paying rent is its own cost. Run both scenarios before you decide.

Compare loan cost scenarios using the CFPB mortgage calculator

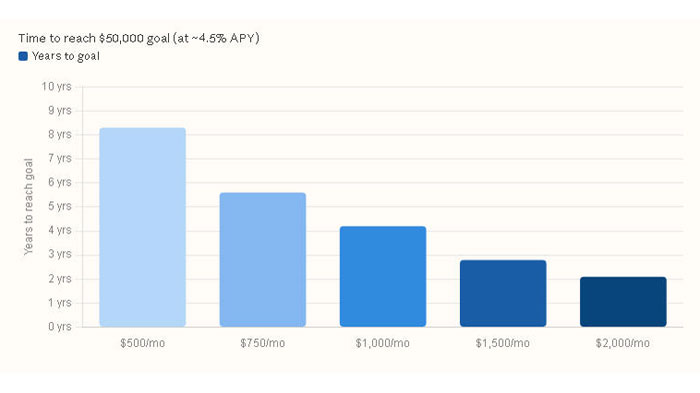

How Long Will It Realistically Take?

| Monthly Savings | Target: $50,000 |

|---|---|

| $500/month | ~8.3 years |

| $1,000/month | ~4.2 years |

| $1,500/month | ~2.8 years |

| $2,000/month | ~2.1 years |

This assumes a high-yield savings account at ~4.5% APY. Small increases in your monthly contribution cut years off your timeline.

8 Proven Strategies to Save Money for a House

1. Automate Your Savings First

Set up an automatic transfer on payday — before you touch your paycheck. This is the single highest-impact change most buyers can make.

The logic is simple: money you never see, you never spend.

Open a savings account used only for your home fund. Name it something concrete — “Home 2027” works better psychologically than “Savings Account 2.” Research in behavioral economics consistently shows that labeled accounts reduce the chance of unplanned withdrawals.

2. Use a High-Yield Savings Account — Not Your Checking Account

Parking your down payment savings in a standard checking account is a mistake. As of early 2025, top high-yield savings accounts (HYSAs) are offering 4.50%–5.00% APY — compared to the national average savings rate of just 0.46%.

| Account Type | Typical APY | On $20,000 After 1 Year |

|---|---|---|

| Standard Savings | 0.46% | +$92 |

| High-Yield Savings | 4.75% | +$950 |

That gap compounds. Put your money to work while you save.

Learn how to compare the best high-yield savings accounts for your goals

3. Audit Your Three Biggest Expenses

Cutting your daily coffee saves $150/year. Cutting your car payment, rent, or subscriptions saves $3,000–$10,000/year.

According to the Bureau of Labor Statistics Consumer Expenditure Survey, housing, transportation, and food account for over 70% of the average American household’s spending. That’s where the money is.

Start with:

- Housing: Can you temporarily move somewhere cheaper, get a roommate, or refinance?

- Transportation: Could you downsize to one car or refinance your auto loan?

- Subscriptions: Audit every recurring charge — most households pay for 3–4 services they rarely use

4. Redirect Windfalls Directly to Your House Fund

Tax refunds, work bonuses, freelance income, and cash gifts are powerful savings accelerants — if you treat them as house money before you spend them.

The average federal tax refund in 2024 was $3,011, according to IRS data. Depositing that directly into your HYSA instead of lifestyle spending cuts months off your timeline.

5. Build a Side Income Stream

A second income stream doesn’t need to be a second job. Even $300–$500/month in side income changes the math significantly:

- Freelance writing, design, or consulting

- Selling unused items (Facebook Marketplace, eBay)

- Renting a spare room on Airbnb

- Tutoring or teaching an online skill

6. Pause Retirement Contributions — Carefully

Redirecting 401(k) contributions to your house fund can accelerate savings. But this decision carries real costs.

⚠️ Risk Callout — Read Before You Act:

- If your employer matches contributions, pausing means losing free money

- You lose compound growth permanently on paused contributions

- Early 401(k) withdrawals (not pauses) trigger a 10% penalty plus income tax

Recommended approach: At minimum, keep contributions up to your employer’s match. Only consider pausing contributions above that threshold — and only after you have a 3–6 month emergency fund in place. Consult a certified financial planner (CFP) before making this call.

7. Explore Down Payment Assistance Programs

Most first-time buyers don’t know these programs exist.

Federal options include:

- FHA loans: 3.5% down with a 580+ credit score

- VA loans: 0% down for eligible veterans and service members

- USDA loans: 0% down in qualifying rural areas

Beyond federal programs, most states offer Down Payment Assistance (DPA) — grants or low-interest loans that can cover part of your down payment. The average DPA award is $17,000, according to Down Payment Resource.

Search your state’s available down payment assistance programs

Roth IRA bonus: First-time buyers can withdraw up to $10,000 in Roth IRA earnings penalty-free. Consult a CPA before using this — the rules are specific.

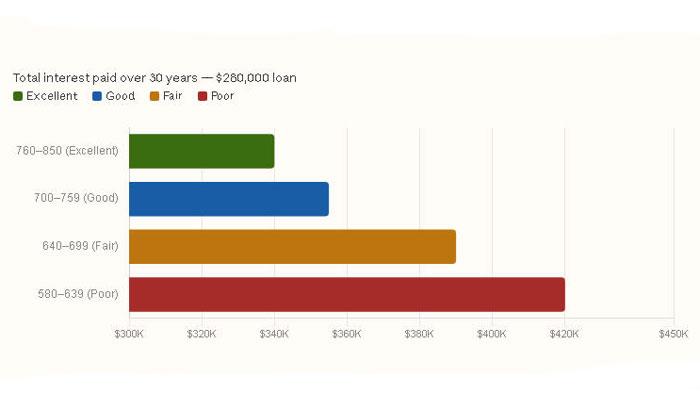

8. Protect and Improve Your Credit Score Now

Your credit score doesn’t just determine whether you get a mortgage — it determines how much you pay for it.

| FICO Score | Estimated Rate | Total Interest (30yr, $280K loan) |

|---|---|---|

| 760–850 | 6.4% | ~$340,000 |

| 700–759 | 6.6% | ~$355,000 |

| 640–699 | 7.1% | ~$390,000 |

| 580–639 | 7.5% | ~$420,000 |

A 120-point difference in credit score can cost you $80,000+ over the life of a loan.

Start at least 6 months before applying for a mortgage:

- Pay down revolving credit card balances

- Don’t open new credit accounts

- Dispute errors at AnnualCreditReport.com

- Keep old accounts open to preserve credit history length

Common Mistakes That Derail First-Time Buyers

- Saving only for the down payment — closing costs and reserves blindside them

- Keeping savings in a regular checking account — losing thousands in potential interest

- Ignoring credit score until mortgage application time — too late to fix

- Investing the down payment in stocks — market timing risk right before you need the money

- Not researching DPA programs — leaving free money on the table

Frequently Asked Questions

It depends on your target amount and monthly savings rate. Saving $1,000/month toward a $50,000 goal takes about 4 years in a high-yield savings account at 4.5% APY. Boosting income or cutting expenses can cut that timeline significantly.

It depends on your target amount and monthly savings rate. Saving $1,000/month toward a $50,000 goal takes about 4 years in a high-yield savings account at 4.5% APY. Boosting income or cutting expenses can cut that timeline significantly.

If your timeline is under 3 years, keep the money in a high-yield savings account — market volatility is too risky for short-term goals. If your timeline is 5+ years, a conservative investment approach may make sense. Talk to a financial advisor before deciding.

You can take a loan from your 401(k) — not a withdrawal — which avoids the 10% penalty. However, you’ll need to repay it with interest, and if you leave your job, the loan often becomes due immediately. Withdrawals (not loans) are generally not penalty-free except under hardship provisions.

It depends on your target amount and monthly savings rate. Saving $1,000/month toward a $50,000 goal takes about 4 years in a high-yield savings account at 4.5% APY. Boosting income or cutting expenses can cut that timeline significantly.

Disclaimer

The content in this article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Mortgage rates, program eligibility, and financial regulations change frequently. Always consult a licensed financial advisor, certified financial planner (CFP), or HUD-approved housing counselor before making major financial decisions related to home buying.