If you’re sitting on a significant chunk of cash — from a year-end bonus, an inheritance, or proceeds from a property sale — and wondering whether to apply it to your mortgage, you’re asking exactly the right question. With 30-year fixed mortgage rates still elevated well above the historic lows millions of Americans locked in during 2020–2021, refinancing frequently doesn’t pencil out. But there’s a lesser-known strategy that could meaningfully cut your monthly payment without touching your rate: mortgage recasting.

This guide explains exactly how recasting works in 2026, who qualifies, what it costs, and — most importantly — when it makes financial sense versus when your cash is better deployed elsewhere.

Key Takeaways

- Mortgage recasting lets you make a large lump-sum payment toward your principal, after which your lender recalculates your monthly payment at the same interest rate and remaining loan term.

- Unlike refinancing, recasting requires no credit check, home appraisal, or closing costs — fees typically run just $150–$500.

- Only conventional loans are eligible; FHA, VA, and USDA loans do not qualify.

- As of early 2026, an estimated 70%+ of outstanding U.S. mortgages carry rates below 5%, per Federal Housing Finance Agency data — making recasting far more compelling than refinancing for most existing homeowners.

- Recasting permanently reduces your required monthly payment but does not shorten your loan term or move up your payoff date.

How Does Mortgage Recasting Work?

Mortgage recasting — also called reamortization — is a process where you make a substantial one-time payment directly toward your loan principal, and your lender recalculates your monthly payment based on the new, lower balance. Your interest rate, loan term, and payoff date remain completely unchanged.

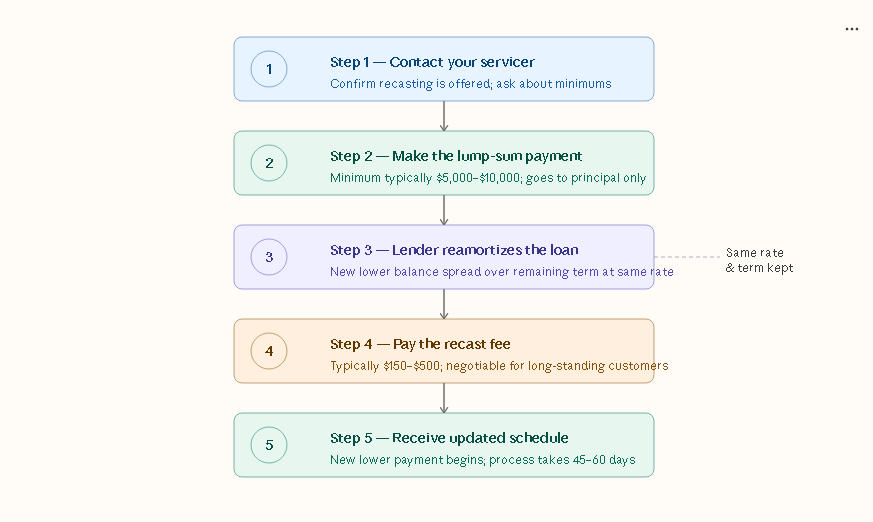

Here’s the step-by-step process:

- Contact your servicer to confirm recasting is available on your loan and ask about minimum payment thresholds (typically $5,000–$10,000).

- Submit the lump-sum principal payment. Every dollar goes directly toward reducing your outstanding balance.

- Your lender reamortizes the loan — spreading the new, lower balance over your remaining term at the existing rate.

- Pay the recasting fee, if applicable. Most lenders charge between $150 and $500.

- Receive your updated amortization schedule, typically within 45–60 days.

💡 Pro Tip: Before you call your servicer, pull your most recent mortgage statement and note your exact current principal balance and remaining term in months. Walking in with those numbers speeds up the conversation and signals you’re a prepared borrower — which can matter when negotiating the recast fee.

Mortgage Recasting vs. Refinancing: The 2026 Rate Reality

This is the comparison that matters most right now. Context is everything.

| Factor | Recasting | Refinancing |

|---|---|---|

| Interest rate | Stays the same | Resets to current market rate |

| Loan term | Unchanged | Can shorten or extend |

| Credit check required | No | Yes |

| Home appraisal required | No | Usually yes |

| Upfront cost | $150–$500 flat fee | 2%–6% of loan amount |

| Monthly payment | Decreases | Depends on new rate/term |

| Payoff timeline | Unchanged | Can change |

| Best for | Rate already low; want lower payment | Rate environment meaningfully improves |

The arithmetic is stark: if you secured a 2.875% or 3.25% mortgage in 2020–2021 and current 30-year fixed rates sit in the 6.5%–7.0% range (per Freddie Mac’s Primary Mortgage Market Survey, early 2026), refinancing would nearly double your interest rate and balloon your monthly payment. Recasting lets you preserve that below-market rate while reducing your monthly obligation.

💡 Pro Tip: If your servicer quotes a recasting fee above $500, push back — especially if you’ve been a customer for five or more years with a spotless payment record. Several major servicers routinely waive or reduce fees for long-standing borrowers. It takes one phone call and costs nothing to ask.

Mortgage Recasting vs. Making Extra Principal Payments

Both strategies reduce your outstanding balance and lower total interest paid — but they serve fundamentally different goals.

Extra principal payments offer flexibility. You can add $300 to your payment one month and skip the extra the next. Over time, the cumulative effect shortens your loan term — but your required minimum payment never changes.

Recasting is the opposite trade-off: you commit a large sum upfront, and in exchange, your required monthly payment drops permanently for the remainder of the loan — improving your cash flow every single month.

“For homeowners approaching retirement who want to reduce fixed monthly obligations without surrendering a favorable rate, recasting is often the most elegant and underutilized solution available,” says Keith Gumbinger, vice president at HSH Associates, a leading mortgage research firm.

When extra payments beat recasting: If you’re uncertain how long you’ll stay in the home, or if you’d rather keep your cash accessible, incremental extra payments preserve liquidity while still building equity. They also accelerate your payoff date — recasting does not.

Real-World Example: What Recasting Actually Saves You

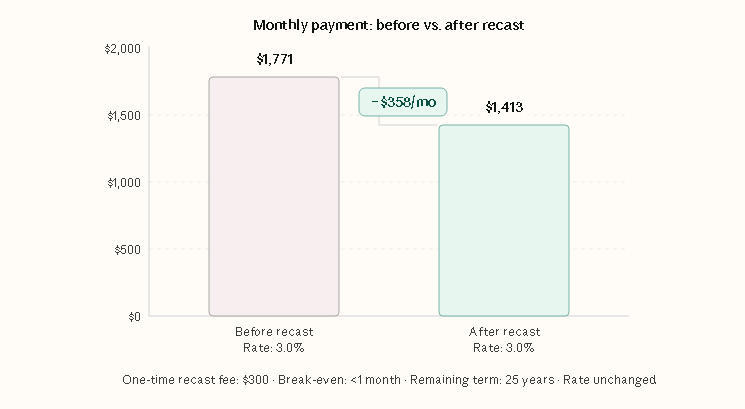

Take Marcus, a 41-year-old project manager in Denver, Colorado. In 2021, he purchased his home with a 30-year mortgage of $420,000 at 3.0%. His monthly principal-and-interest payment: $1,771.

In early 2026, after receiving a significant inheritance, he found himself with $75,000 available. With prevailing rates near 6.8%, refinancing would have pushed his payment to roughly $2,700/month — nearly $930 more per month and tens of thousands in closing costs. Instead, Marcus initiated a recast with his servicer.

| Before Recast | After Recast | |

|---|---|---|

| Remaining balance | $372,000 | $297,000 |

| Interest rate | 3.0% | 3.0% |

| Remaining term | 25 years | 25 years |

| Monthly payment | $1,771 | $1,413 |

| Monthly savings | — | $358 |

| Recast fee paid | — | $300 |

Marcus’s break-even on the $300 fee: less than one month. And he preserved his 3.0% rate for the next 25 years.

💡 Pro Tip: Model your recast scenario with a mortgage amortization calculator before calling your servicer. Input your current balance, remaining months, existing rate, and proposed lump-sum amount. Arriving with a pre-calculated estimate prevents surprises and lets you evaluate the servicer’s numbers independently.

How to Qualify for Mortgage Recasting in 2026

Not every borrower — or every loan — is eligible. Here’s what servicers typically require:

- Conventional loan only: FHA, VA, and USDA loans are ineligible for recasting under current agency guidelines. Jumbo loans may qualify, but availability varies by lender — confirm directly.

- Minimum lump-sum payment: Usually $5,000–$10,000, though high-balance loans may require more.

- Clean payment history: Most servicers require at least 2–6 consecutive months of on-time payments before approving a recast request.

- Minimum equity threshold: Some lenders require 10%–20% remaining equity after the lump-sum is applied.

- Loan not in forbearance or modification: Active loss-mitigation arrangements typically disqualify you immediately.

Pros and Cons of Mortgage Recasting

Pros:

- Permanently reduces your required monthly payment without refinancing costs or rate risk

- Preserves your existing (likely below-market) interest rate

- No credit inquiry, no appraisal — minimal paperwork and friction

- Reduces total lifetime interest paid on the loan

Cons:

- Requires a large, illiquid commitment of cash upfront

- Does not shorten your loan term or accelerate your payoff date

- Unavailable on government-backed loans (FHA, VA, USDA)

- Not offered by all servicers — availability is inconsistent across lenders

Should You Recast Your Mortgage? A 2026 Decision Framework

Consider recasting only if all of the following apply:

- Your loan is conventional and your servicer explicitly offers recasting.

- Your current interest rate is materially below today’s prevailing rates (making refinancing a net negative).

- The lump sum won’t deplete your emergency fund — most certified financial planners recommend keeping 3–6 months of living expenses liquid.

- You carry no high-interest debt (credit cards, personal loans at 15%+ APR) — paying those off first delivers a higher guaranteed “return.”

- You’d value lower monthly obligations over a faster payoff timeline.

If any of those conditions don’t hold, recasting may not be the optimal use of your capital. A $75,000 recast saving $350/month is mathematically less valuable than eliminating $20,000 in credit card debt at 22% APR — the guaranteed interest savings from the latter are simply larger on a risk-adjusted basis.

FAQ

Call your loan servicer directly — recasting is rarely advertised proactively. Large national banks and many credit unions offer it; some smaller non-bank servicers do not. If your current servicer doesn’t offer recasting, that’s worth factoring into any future refinance or loan-transfer decision.

Most lenders require a minimum lump-sum of $5,000 to $10,000. Higher-balance jumbo loans may set a higher threshold. The larger your payment, the more significant your monthly savings — but any amount above the minimum will reduce your balance and interest costs proportionally.

No. Unlike refinancing, recasting involves no hard credit inquiry and no new loan origination. It has zero impact on your credit report or score.

From submitting your lump-sum payment to receiving your updated amortization schedule, the full process typically takes 45 to 60 days. You’ll continue making your existing monthly payment during that window.

No. Government-backed loans — including FHA, VA, and USDA mortgages — are not eligible for recasting under current federal agency guidelines. Only conventional loans (and potentially some jumbo loans, depending on the servicer) qualify.

Disclaimer: The information in this article is intended for educational and informational purposes only and does not constitute financial, mortgage, legal, or investment advice. Individual financial circumstances vary significantly. Readers should consult a licensed mortgage professional, certified financial planner (CFP), or qualified legal advisor before making any decisions regarding their mortgage or personal finances.