CD Interest Calculator By Month

Use our free CD Calculator to instantly estimate your certificate of deposit earnings. Enter your deposit, term, and APY to compare returns vs. the national average.

Frequently Asked Questions

Free CD Calculator: enter your deposit, term, and APY to see projected earnings and compare your CD returns against the national average in seconds.

A Certificate of Deposit is a savings product offered by banks and credit unions that pays a fixed Annual Percentage Yield (APY) in exchange for keeping your money deposited for a set term — typically ranging from 3 months to 5 years. Unlike a regular savings account, you agree not to withdraw the funds early; in return, you generally receive a higher, guaranteed interest rate. CDs are insured by the FDIC (banks) or NCUA (credit unions) up to $250,000 per depositor, making them one of the safest ways to grow your savings.

Enter three inputs: your Initial Deposit (the lump sum you plan to invest), the Term (how long you'll keep the CD, in months or years), and the APY (Annual Percentage Yield quoted by your bank). The calculator applies monthly compound interest using the standard formula:

Balance = Principal × (1 + APY/12)^months

It then displays your total balance, total interest earned, and a year-by-year comparison chart showing your projected earnings versus the national average APY — so you can instantly see how much more a competitive rate is worth.

APY (Annual Percentage Yield) reflects the real rate of return after accounting for compounding interest within the year. APR (Annual Percentage Rate) is the simple annual rate without compounding. For CDs, banks are legally required to advertise APY, which makes comparison shopping straightforward. A CD advertised at 3.15% APY will always earn exactly 3.15% on your principal over 12 months, regardless of how often interest is compounded internally.

As of 2025, the FDIC-reported national average APY for a 12-month CD hovers around 0.50%–0.60%. However, online banks and credit unions regularly offer rates of 4.00%–5.50% APY — often 4× to 8× higher than the national average. This calculator uses 0.57% as the national average benchmark so you can visually compare what you'd earn at your bank versus a top-yielding CD.

Most CDs compound interest monthly, though some compound daily or quarterly. The more frequently interest compounds, the slightly higher your effective yield. This calculator uses monthly compounding, which is the most common standard. Always confirm the compounding frequency with your bank, as it affects your final payout — especially on longer-term CDs.

CDs carry an early withdrawal penalty (EWP) if you redeem before the maturity date. The penalty typically equals several months of interest — for example, 90 days' interest on short-term CDs and up to 150–365 days' interest on multi-year CDs. This calculator assumes you hold the CD to full maturity. If early access to funds is possible, consider a no-penalty CD or a high-yield savings account instead.

The Months tab lets you calculate short-term CDs (e.g., a 6-month or 18-month CD). The Years tab is ideal for standard terms like 1, 2, or 5 years. Simply click the tab that matches the term quoted by your bank, enter the number, and the calculator updates the chart and results in real time. Both modes support decimal inputs — for example, enter "1.5" in Years mode for an 18-month CD.

Minimum deposit requirements vary by institution. Traditional banks often require $500–$1,000 to open a CD, while some online banks have no minimum. Brokered CDs (purchased through investment platforms) may require $1,000 or more. This calculator accepts any deposit amount — use it to model different scenarios before committing your funds.

Yes. CDs held at FDIC-member banks are insured up to $250,000 per depositor, per institution, per ownership category. CDs at NCUA-member credit unions carry equivalent protection. This means your principal and accrued interest are fully protected up to the limit even if the bank fails — making CDs one of the lowest-risk investment vehicles available to individual savers.

Choose a CD if you have a specific savings goal with a known timeline (e.g., a down payment in 2 years) and want a guaranteed, locked-in rate that won't drop if the Fed cuts rates. Choose a HYSA if you need flexibility and liquidity — HYSA rates are variable and can fall, but you can withdraw at any time without penalty. Many savers use both: a HYSA for their emergency fund and CDs for medium-term goals.

Latest News

Focus on rapid changes in the global market, keeping up with the latest financial trends and major market news.

How to Save Money as a Kid: A 2026 Parent’s Guide

Learning how to save money as a kid shapes financial habits that last a lifetime. Raising a child now…

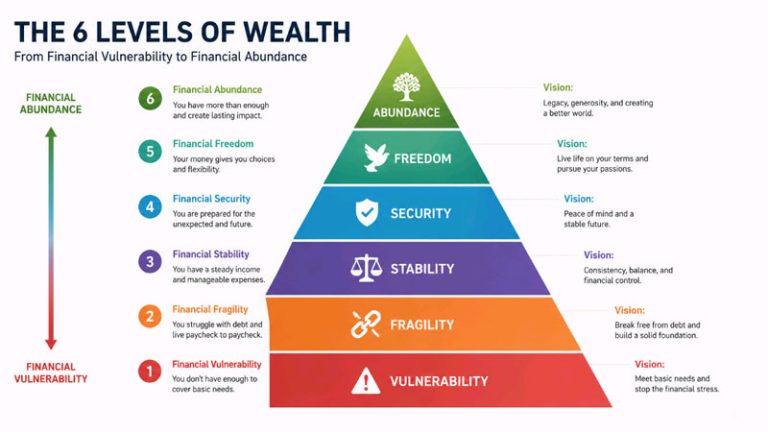

The 6 Wealth Levels: Where Do You Really Stand in 2026?

Most people confuse being rich with being wealthy. Wealth levels aren’t about your paycheck or your car lease. They’re…

Bad Credit Loan Myths That Cost You Money in 2026

Bad credit loan myths keep good borrowers stuck with bad choices. A low score doesn’t lock every door —…